Tax Alpha and Moral Decay

What Wall Street's New Cash Cow says about the rise of Trumpism

I’m a keen reader of Matt Levine’s Money Stuff newsletter. It has taught me a lot, both about how the finance industry works, and clear communication in general. As I have been blogging in one form or another for the past few years, I would hope that his influence has helped me to explain some of the more complex ideas I have touched on.

A trend that he has noticed over the past few years is that—in most cases—investment managers are finding it harder and harder to charge high fees for their specific investment decisions. Alpha (above market risk-adjusted returns) is fleeting, and their clients have begun to rightfully ask what they are paying for, as the disclaimer at the end of every ad for an investment product notes, “past performance is no guarantee of future results.”

But, investment managers are a tenacious lot and they have plenty of resources at their disposal. And they understood the nebulous nature of their alpha long before their clients did. So, some of the smartest minds in finance, noting the chasm that exists between tax law and economics realities, realized it is a lot easier to generate market-matching returns with a reduced tax liability. And then they could charge fees based on the tax savings. After all, tax savings are structural. Luck should play no part. alpha generated by investment skill, such as it exists, which investors would be more willing to pay for.

Over the last year alone, strategies like this have surged with AQR capital management—a pioneer of the approach despite their posturing of academic rigor—seeing its AUM in the strategy going from $10 billion to $45 billion, and everyone from WorldQuant to the House of Morgan jumping into it.

Here’s how the basic version works. You own Stock A, it’s down 10%, you sell it, book the tax loss, immediately buy Stock B which is basically identical. The wash sale rule says you can’t buy the same stock for 31 days, but a different ETF tracking the same index? Totally fine. You maintain your market exposure, but now you have a tax loss to offset gains elsewhere. Repeat this across hundreds of positions and you can generate meaningful savings year after year.

There are more sophisticated versions. One that fills me with rage was launched in July 2025, by Roundhill Investments. The S&P 500 No Dividend Target ETF. The fund tracks the S&P 500 by investing in other ETFs tracking the S&P, but whenever one is about to pay a dividend, XDIV transfers its position into a different one that isn’t. Economically, you own the S&P 500. For tax purposes: you haven’t received any dividends. The product exists purely to create a gap between reality and what you report to the IRS.

This type of work has been immensely profitable, both for the finance industry and for the investors who have avoided many billions of dollars in taxes as a result. But it is not victimless. Firstly, that revenue loss has to be made up in borrowing, which has to be paid back with interest. Secondly, it involves operating in a grey area, both for investors and managers. Now broken window theory isn’t exactly my favorite theory of criminal justice, but I am too much a connoisseur of financial shenanigans not to have noted how thin the line between aggressive interpretations of statutes and outright criminality can be. And as much more favorable towards innovation in the financial sector I am than the average Democrat, even I struggle to intuit benefits in terms of capital allocation or market efficiency from what are functionally wash trades.

The fact that society accepts this behavior has been deeply damaging. My 18th birthday occurred a few days before Donald Trump took his fateful journey down his gold plated elevator to announce his presidential campaign. And while there were problems with American society before then, I do not imagine I am alone in noting that a moral rot has taken hold within a certain portion of the American character. And I see aggressive tax avoidance, of which Trump is a gleeful participant, as integral to that rot.

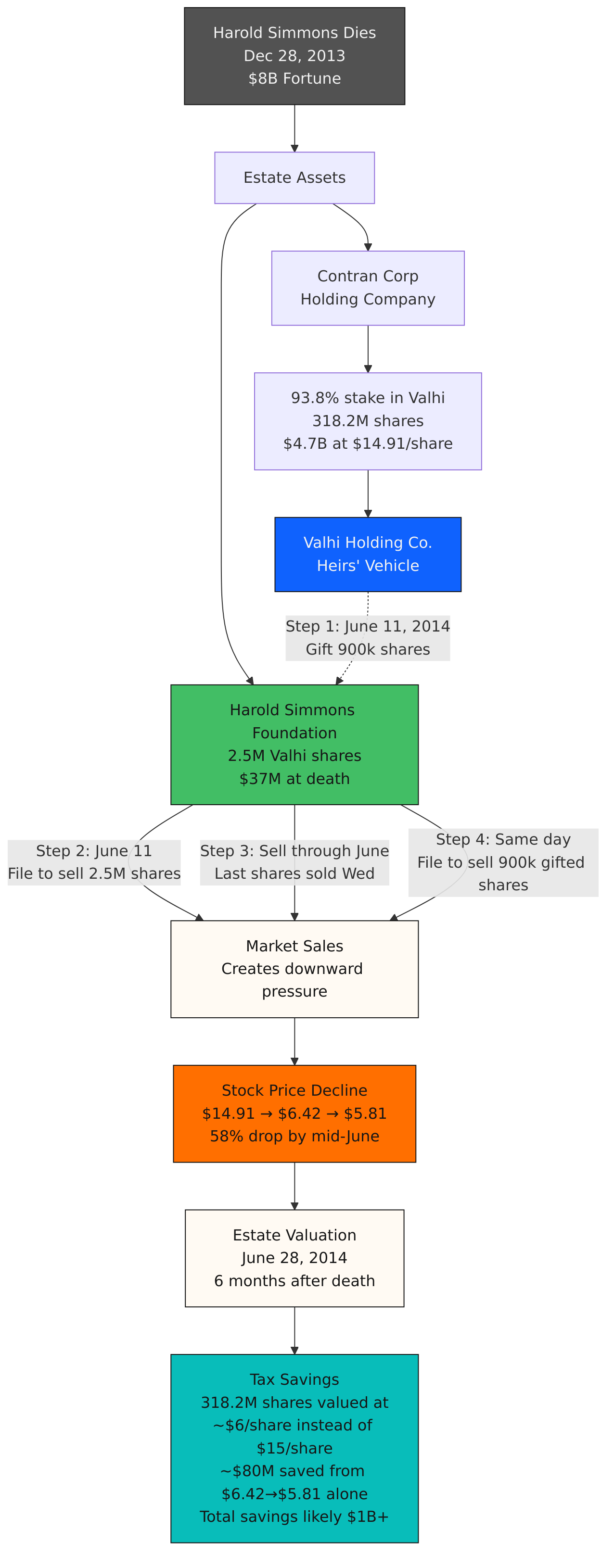

To support this opinion, it seems like now is the right time to turn to Trump’s former close personal friend Jeffrey Epstein. Specifically, it deals with a 2013 scheme by a Texas Billionaire and his family to avoid around a billion dollars in estate taxes by flooding the market with shares of a thinly traded company to cut the estate valuation. Because, once again, I am a connoisseur of financial shenanigans, I have included a brief summary of the scheme in the below diagram, with a link to a proper write up in the caption.

In January 2014, Levine wrote a Bloomberg opinion piece about the scheme, which came to the attention of a trusts and estates lawyer at the white-shoe firm Paul, Weiss, Rifkind, Wharton & Garrison LLP. Yes, it is the same Paul Weiss that folded immediately to the Trump administration’s lawless intimidation of law firms earlier this year. Seeing the scheme, the lawyer emailed Epstein saying, “I thought of you when I read this. Was this your idea?”

I think Levine sums up the situation better than I could:

In the early days of the Epstein scandal, one mystery that bothered me and a lot of other people was: Where did his money come from? A small collection of billionaires seemed happy to pay him hundreds of millions of dollars, but for what? Given the context, there were various wild theories, but as far as I can tell the answer was just that he was really good at saving them taxes. I once wrote, somewhat jokingly, that Epstein would find tax schemes and then “the fancy lawyers in the Paul Weiss tax department would say ‘wow ... this is amazing, why didn’t we think of this, this guy is a Michelangelo of tax minimization?’” Apparently that really happened!

If, as seems likely, this is at least part of the truth, it fits with my thesis. Leon Black was willing to associate with a post-conviction Epstein because he saw the potential billion dollars in tax savings as worth funneling tens of millions of dollars to a convicted child sex offender. That is moral rot if I have ever seen it.

The difference between aggressive tax planning and enabling crime isn’t hard and fast. And with the incentives that exists, Wall Street will continue to aggressively pursue tax alpha. With Charlie Munger’s wisdom, “show me the incentives and I’ll show you the outcome,” it is clear that the incentives have to be changed. And while this post is already too long for that, I would start by trying to reconcile the tax code to economic reality.