The Estate Tax is Basically Optional. Changing that would Benefit us All

Let's fix things before a new American aristocracy is entrenched

Theoretical congressional candidate and Nepo-baby extraordinaire Jack Schlossberg recently came out in favor of what Jordan Weissmann accurately described as “garden variety NIMBY bullshit,” and “exhibit A for why we need an inheritance tax.” And given that writing a too-long, pie in the sky, tax proposal in response to a tweet is what I do here, the opportunity to write about the inheritance tax seemed too good to miss. In theory, the estate tax is the one of the most efficient and progressive parts of our tax code. A 40 percent levy on the estates left behind by the ultra rich, what isn’t to love?

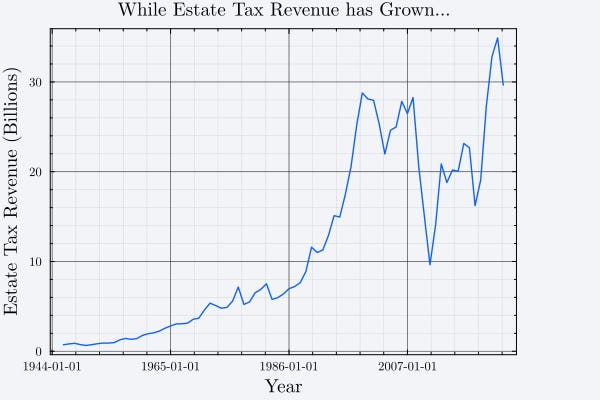

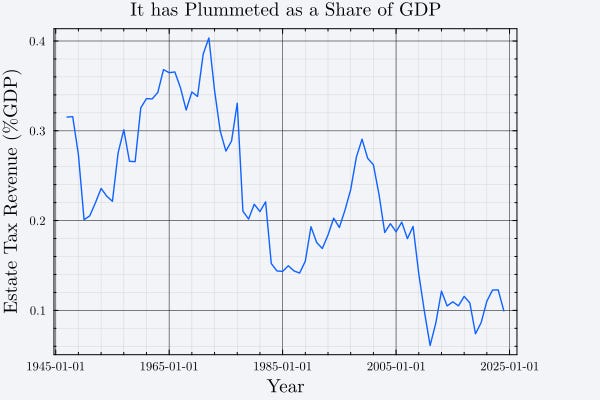

As it turns out, pretty much everything. Persistent lobbying campaigns and aggressive legal work have made it functionally optional. Around four thousand1 estates pay it each year, a time period in which almost three million Americans die. Of the $1.2 trillion transferred between generations each year, only around $32 billion is captured by it.2 It doesn’t work. In the early stages of the largest3 wealth transfer in human history, with the national debt a problem that is just getting worse4, now seems as good a time as any to work on solutions.

Cerulli estimates5 that there will be $124 trillion in inheritances and gifts passed on to younger generations by 2048. It was published in December 2024, and nothing in the last year has led me to believe that the current concentration of wealth will diminish by the time the youngest baby boomers reach their mid 80s. Half of that will be passed to the top 2 percent of households.

Still, a statutory tax rate of 40 percent on $124 trillion over two and a half decades is nothing to sneeze at from a revenue perspective. That’s in the ballpark of trillions of dollars a year. Even at the CRS’6 observed effective rate of 9.2 percent, that would be hundreds of billions more than the roughly $30 billion we currently take in. Unfortunately, however, the edifice of exemptions and avoidance mechanisms that have been put together over the last few decades have ripped the teeth out of the estate tax and cemented the conditions for an unproductive American aristocracy.

For starters, it kicks in way too late. After Trump’s latest round of tax cuts for the rich (the OBBBA) permanently raised the threshold for it to kick in to an astronomical $15 million (and twice as much for married couples). Even at the comparatively progressive threshold of $5.5 million ($11 million for married couples) before Trump’s first round of tax cuts for the rich, only 507 farms and small businesses were subject to it. At current levels, for a married couple to have a bill of $1 million in estate taxes owed, they would need to leave behind a fortune of $32.5 million (an effective rate of barely more than 3%), without having taken advantage of any of the many well worn work around that are described below.

Starting with the mechanism Sheldon Adelson used to avoid8 around $2.8 billion in taxes: Grantor Retained Annuity Trusts (GRATs). The way a GRAT works is that you (the grantor) create an irrevocable trust and transfer an asset into that trust. That trust has to make annuity payments to you based on a rate set by the treasury (120% of the average yield of treasury bonds with maturities between three and nine years), and any appreciation of the asset in the trust above the amount necessary to make the payments can be passed onto an heir tax free. If the asset, for some reason, fails to appreciate faster than the treasury hurdle rate, it just goes back and you can try again. It is a heads I win, tails I break even bet on whether whatever asset you have can outgrow the hurdle rate. Even worse, the trust can be structured in such a way as to “zero out,” and leave the inheritor with no liabilities whatsoever. While data on tax avoidance is hard to tell, but a conservative estimate is that $15 billion in tax avoidance per year is not unreasonable.

A similar concept is the Intentionally Defective Grantor Trust (IDGT). Here, you structure a trust so that it is owned by you for capital gains tax purposes (so that you can sell assets to it without incorporating capital gains), but separate for estate tax purposes (so that any appreciation falls outside of the estate). Somehow, this is legal. Not only is it legal, it costs us at least $8 billion a year.

For families with nonpublic assets, the law allows staggering discounts when making transfers. Minority and lack of marketability discounts can have considerable consequences. Consider a car dealership worth $100 million owned by a married couple with two children. They could set up a family limited partnership where the parents own 1 percent, but act as general partner, while the children each own 49.5 percent as limited partners without management participation rights, or the right to sell without the permission of a general partner. Each of those $49.5 million dollar shares could be discounted by up to 35 percent due to “lack of control,” and then up to another 35 percent due to “lack of marketability”, bringing the value of the $99 million gift to $41.82 million, from which $30 million can be deducted, leading to a tax bill of around $4.73 million. And that is conservative, given how these techniques can be layered. Around $5 billion a year is kept from the taxpayers through these discounts.

The Obama administration tried to place some minor limits on these discounts, but, predictably, the Trump administration withdrew9 those limits in his first year as president.

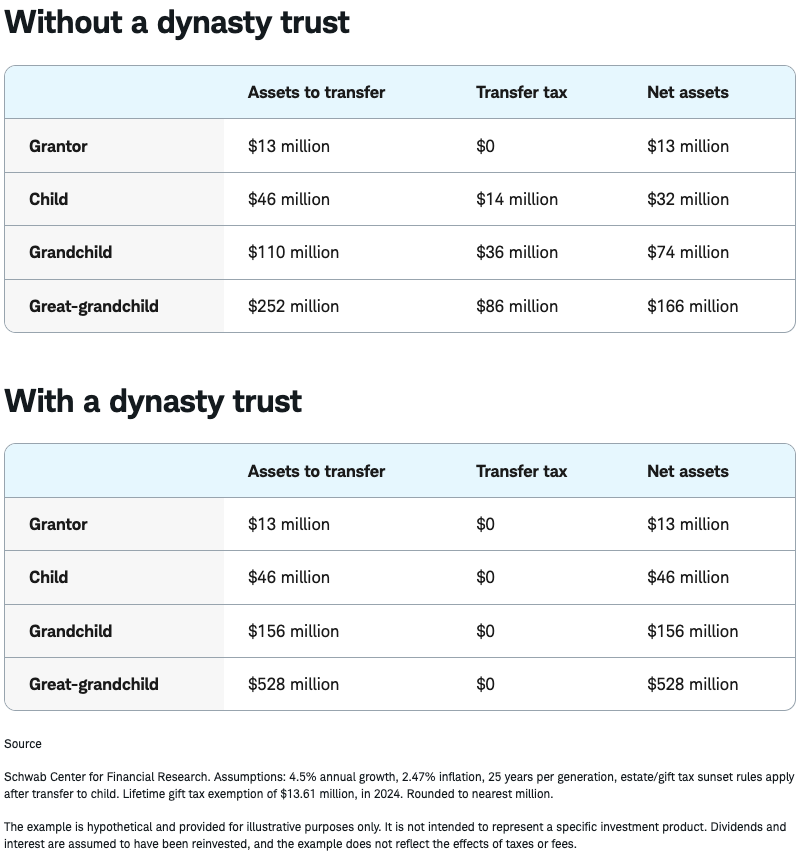

And the well-funded estate planning industry has kept pushing. South Dakota led the way in the reemergence of “Dynasty Trusts,” which allow families to pass assets across unlimited generations without further taxation, ever, as this helpful graphic from Schwab makes clear. These trusts hold at least half a trillion dollars10 in assets, and probably a good deal more given the rise in asset prices since that number was reported. This scale of assets makes it reasonable to assume that at least $10 billion a year in estate taxes are avoided through these structures.

Given the problems I have identified with capital gains tax avoidance, the work that has been done by the estate planning industry has helped to build a world in which productive assets are transformed into the touchstones of a modern aristocracy.

A Three Part Approach

The failures of the estate tax should not come as a revelation. Every meaningful attempt at reform has failed. The Clinton administration’s 1997 proposal to eliminate non-business valuation discounts died in committee. The Obama administration’s eight proposals (on in every Greenbook) on GRAT restrictions were never taken up by Congress. Every estate tax provision in the Build Back Better Act was stripped out before it became the IRA.

Part 1: Close the Loophole

Still, it is necessary to keep working on those changes. While closing the avoidance channels is—in my view—insufficient to fixing the estate tax, it is absolutely necessary. Much of this work has already been proposed, and it is necessary to keep the fight going.

GRATs should, in line with the Obama administration’s proposals, be reformed to have a minimum term of 10 years, a minimum remainder value that cannot be zeroed out, and a mandatory inclusion in an estate if the grantor dies during the term. They would still involve some tax shifting, but at least they would not be risk free to the grantors.

IDGTs should be fundamentally broken down to remove the false distinction between ownership and tax ownership. Meanwhile, valuation discounts should be reanchored in reality. This step may be costly from an administrative perspective, but as I go over later, the expected ROI on this policy mix is such that the cost of robust enforcement is not prohibitive.

A federal law against perpetuities preempting state laws should be enacted. There is no reason for a republic to allow for the creation of trusts that last more than three generations. Furthermore, when the beneficiaries of trusts change, that should count as a taxable event.

Combining these with my proposal for capital gains taxation would eliminate the issue of stepped up basis at death, and make buy, borrow, die moot.

Part 2: Tax Receipts, Not Estates

Currently, the estate tax is levied on the total estate before distribution. That makes some sense. The assets and liabilities are all there, and can be assessed in one go. Still, I think that we can do better. We can tax recipients separately, with each heir facing their own rate based on what they receive.

If the concentration of wealth among a small group of inheritors is something we want to avoid, then our tax system should say that leaving two children $25 million each is worse than leaving two children and eight grandchildren $5 million each. While the current system is indifferent, a receipts-based system wouldn’t have to be. Especially under a system of progressive rates (more on that in the next section).

Wealthy families would face a tradeoff: concentrating control, or reducing taxes. In other words, they could disperse their money, or the government would do it for them. This creates many opportunities for gaming, but so long as it could aggregate lifetime receipts—gifts plus inheritances from all sources—it would result in a substantial improvement.

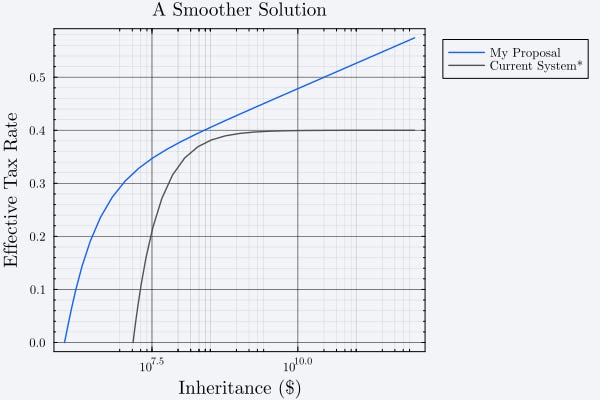

Part 3: Replace the Cliff with a Curve

In theory, the current estate tax is a flat 40 percent. This discontinuity is sharp, and provides incentives for avoidance (just like any tax cliff system). While discrete tax brackets make sense in a world where everyone is doing their taxes by following along with a worksheet, a simple formula proves much harder to game. What I propose is, following a $1 million lifetime deduction, all gifts and inheritances should be taxed according to:

where ϕ is the golden ratio: around 1.618. If you look at the plot below, you can see that the rate is increasing as the inheritance goes up smoothly and continually, although at a decreasing rate.

All Together

Going back to the car dealership worth $100 million owned by two parents with two children. By closing the loopholes used would leave $70 million of the estate taxable, which at current rates means that $72 million would be passed on, $36 million to each child. With the smooth rate structure and tax on receipts, however, things get more interesting. If the parents wanted to leave the estate equally to the children, each one would have $49 million in taxable liability, at a rate of around 36.79 percent, each child would get about $31.96 million. If, however, the parents decided to leave $17 million to each of their children, and $16.5 million to each of their four grandchildren, things get more interesting. After taxes, each of the children would receive ~$11.49 million, and each of the grandchildren would receive ~$11.17 million. By splitting up the inheritance, the parents were able to reduce their tax bill by almost 6 percent.

The family benefits, and society benefits. The “Carnegie conjecture,” that inherited wealth reduces heirs’ productivity is well founded in the economic literature. Furthermore, inheritance can, in some ways, be seen as the ultimate economic rent. This can be seen in the rent-seeking behavior of the Mellon family, who made their money in the early days of the Grant administration, and have done nothing of value to the country (save Andrew Mellon’s exemplary job as a caricature of what FDR was campaigning against), and yet until Elon Musk’s late spending, Thomas Mellon was11 on track to be the top donor in the 2024 cycle.

No one in the Mellon family earned that fortune, nor did anyone in Jack Schlossberg’s generation earn12 the following necessary to mount a congressional campaign. They did it as the result of a policy failure that has stunted social and economic mobility, and brought about an American aristocracy. The time to do something about it is now. Or in 100 years, our descendants will despair at the continued domination of dynasties founded before the advent of Trumpism, just as we despair at the continued power of dynasties founded before the Great Depression.

See Jordan Weissmann in The Argument here

I enjoyed this. Could talk about tax policy for estate/gift tax all day! One of the most underappreciated tradeoffs in estate planning, in my view, is that assets transferred out of the estate through a GRAT or IDGT escape estate tax but carry their original cost basis — the heirs inherit the embedded gain along with the wealth. Assets that stay in the estate get a full step-up at death, wiping out decades of appreciation entirely. For families where estate tax is inevitable regardless, the calculus on aggressive transfer planning gets more interesting. Basis planning deserves more attention than it gets.