Zero Interest is a (Bad) Policy Choice

The time to fix capital gains taxes has come

I am normally something of a fan of Alexis Ohanian. Despite having clearly spent too much time in Silicon Valley, and horrible taste in soccer teams, reddit and Athlos are endearing creations. But at the end of last year, he shared this tweet, which got me thinking about how poisoned the discourse around capital gains is. So I thought it was a good opportunity to go over the mess that is our current system of capital gains taxation, and its most important flaw, which Ohanian and his ilk idolize: deferred obligations.

When you open a position with $100, and it goes up to $200, you have $100 more than you did when you opened the position. But you don’t owe any taxes on that additional $100 until you close the position. To anyone with a brokerage account that seems normal, but the longer you think about it the weirder it is. You’ve gotten $100 richer, and have effectively deployed that $100 to invest. You can, if you want, borrow against that $100, and there is a strong literature suggesting that people make decisions on the basis of having that additional $100.

Meanwhile, the government has services to provide and those services have costs. So it would like to tax you on that additional $100, like it would with any income realized by any other American. If the tax rate on capital gains is 25%, you owe the government $25 on your gain. But you get to choose when you pay, and because you haven’t closed the position and “realized” the gain yet, it doesn’t collect the taxes you owe on it. You will owe them when you close the position (unless you die beforehand, more on that later), but until then, you can use the money, either by keeping it invested, or by borrowing against the asset it represents. The government is essentially giving you an interest free loan that you get to pay back when you choose.

To continue with this example, let’s say that the next year, the asset grows by 10 percent, so you now have $220. Your capital gains are now $120, and you owe $30. But, because you didn’t pay $25 when you had $100 in gains, it stayed invested and you got an extra $2.50. That’s weird, and with the real capital gains taxation system, things get even weirder.

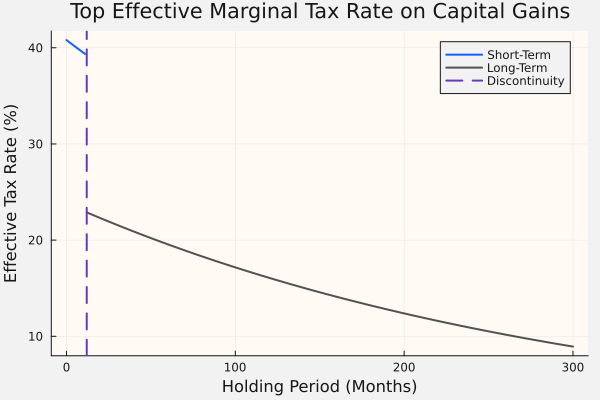

In theory, it depends on the overall level of income realized by an individual, but capital gains are so concentrated at the top, it is safe to work from the assumption of top earners. Assuming they do not engage in the kind of chicanery all too common to that class, capital gains from assets held for less than a year are assessed as ordinary income, up to a rate of 37 percent, with a potential net investment income tax (NIIT) of 3.8 percent, for a total of 40.8 percent on marginal dollars. For assets held for longer than a year, the top marginal dollars of gains are taxed at around rate of 20 percent, although, the NIIT still applies, so it is actually 23.8.

This discontinuity is a major source of tax avoidance. Because there is little economically different between holding a position for 364 or 366 days, it is fairly trivial (as detailed in this ProPublica story) to move gains from short term to long term.

Visualizing the discontinuity between short and long term rates, along with the fact of the unrealized loan gives a system that looks something like this:

But for the very rich, like Ohanian, the good part hasn’t even come yet. That happens when you die. Under current law, when you die, any capital gains are wiped out and the position is transferred to your heirs as if they opened it that day. This is called “stepped-up basis.”

Going back to the earlier scenario, if you die after your position doubles, your heir(s) get it as if it was always worth $200. That isn’t an interest free loan. Those gains were never taxed. They never will be taxed. We have always been at war with Eastasia.

It is even better if you borrow against your assets while you live. For very high net worth individuals, this is a great bet for banks. A small (20-30%) percentage of a large portfolio is very good collateral as stocks rarely decline by enough fast enough for a margin call to not be effective. Then you have plenty of cash, and interest expenses to mop up any pesky net investment income you can’t help but realizing. Then your heirs can sell some of the stepped-up assets to pay off the loans.

I don’t think this is good. It is a major reason the ultrarich pay lower effective tax rates than the upper middle class, it feeds an industry that degrades our moral character, and—arguably most importantly—it misallocates capital.

If you invested $100,000 into one company a decade ago and your position is worth $1 million today, you have $900,000 in unrealized capital gains. If you think another company will do better going forward, you would have to realize those gains and pay around $214,200 in taxes before you could invest in that other one. That means you would be turning a $1 million holding in a company with potentially mediocre prospects to $785,800 in a company with better ones. So that second company would have to dramatically outperform the first one in order for the switch to be worth it.

This means that privately rational investors are not allocating to the best companies anymore. That seems to undermine the point of our modern financial markets.

So here’s what I’d do. I’d stop making the loan interest free. Just pay the taxpayers back for the privilege of holding our money.

For example, if the rate on capital gains was 25 percent, and you had $1 million in unrealized capital gains during a quarter where the average federal funds rate was 3 percent. You would have to pay the taxpayers 0.75 percent (the 3 percent, divided by a quarter) times the $250,000 you would owe on your gain: $1,875.

When you close the position, you will owe the full amount, but until you do, you should have to pay for the privilege of the deferral.

This proposal is, unfortunately a bit too simple, so after some consultation with several LLMs about potential pitfalls and complications, this is what I have come up with to enhance it.

There should be a progressive system on capital gains (like there is today), but with no distinction between short and long term capital gains. A discontinuity that massive is too attractive a target for tax avoidance.

The stepped up basis should be eliminated. Your heirs should have a choice. They can close the position and pay the taxes on the capital gains, or they could continue to pay interest. But they shouldn’t receive a clean slate.

For illiquid or hard to value assets, you should have to make up interest payments at realization on the assumption that the asset grew at a continuous rate during the time you held it, but those payments should be summed without the assumption that they compound. I know this is essentially another interest free loan, but hopefully it would be much less consequential.

Unrealized losses should create a nonrefundable tax credit against other income earned in that current quarter. Honestly, I don’t love this idea, and I would be interested in other ideas, but while the government shouldn’t send you checks because your portfolio is down, there should be some symmetry.

Finally, there should be a floor below which no payments are owed. Assuming the floor is something like $1000 per quarter, that would mean you would need between $400,000 and $800,000 in unrealized gains (depending on the federal funds rate) to have this effect you.

My choice of the federal funds rate was no coincidence. I think it could shorten the “long and variable lags” associated with monetary policymaking.

Rate hikes would bite more as people would see higher carrying costs for their investments. Admittedly, there would be a bit of an asymmetry where the tax relief provided by rate cuts would be smaller than the hit from rate hikes, but given the fact that the relief would be a regressive tax cut, I am ok with it.

I also think it would make markets more efficient. While there would still be some lock in (you still have to pay capital gains on your first position before moving to your second), but I think it would be dramatically improved.

Revisiting the scenario I used to illustrate the problem, with a 3 percent federal funds rate and the same 23.8 percent capital gains rate I used. Now, you’re paying $1,606.5 per quarter to maintain your $900,000 in capital gains. If you sell, you will still owe the $214,200 in capital gains you owe, which would mean you would only have $785,800 to invest in the company you think has better prospects. But, now, making that trade cuts your quarterly bill dramatically as, even with better performance, I would imagine it would take a while to accumulate another $900,000 in capital gains, and the savings from those quarterly payments combined with the improved performance of that second company would, provide some upside to staying locked in.

My proposal wouldn’t fix everything that is wrong with the current system. Real estate would still be a mess (but that would be less of an issue if it were combined with a land value tax). But it would directly address the core problems I have identified. Capital would be better allocated and revenue would be higher.

The way we tax capital gains is currently unfair and inefficient. It rewards behavior that isn’t societally beneficial and creates a network of holes for tax avoidance. If you’re going to defer your obligations to us, the least we can do is charge you interest.